April 7th, 2017

Dear Steward:

As required by Regulation 390/16 under the Ontario Waste Diversion Transition Act, 2016, Ontario Tire Stewardship (OTS) has calculated the costs of diverting used tires per new tire supplied for 2017 based on the actual 2016 tire supply figures and Used Tires Program (UTP) costs. As described in the Regulation the calculation process employed by OTS is to:

(a) determine the cost attributable to each tire class in respect of the base fee period by,

(i) determining the sum of the amounts described in paragraph 1 of subsection 33 (5) of the Act that were incurred in relation to used tires during the cost reference period, and

(ii) determining, subject to subsection (5), the portion of that sum that is attributable to each tire class; and

(b) determine the cost attributable to a tire in each tire class in respect of the base fee period by,

(i) assigning each tire supplied by stewards during the cost reference period to a tire class if the tire meets the criteria of the tire class, and

(ii) dividing the cost attributable to a tire class, as determined under clause (a), by the number of tires assigned to that tire class under subclause (i).

In undertaking the calculation, OTS has included two cost variables that affect the net cost attributable to certain tire classes. These variables are:

1. Historic OTR Deficit premiums/credits: Prior to 2013, the revenues generated from Tire Stewardship Fees (TSFs) on Off-the-Road (OTR) tires were insufficient to cover the costs of diverting these tires. During the same time period, TSF revenues from Passenger & Light Truck (PLT) tires exceeded the costs of diverting these tires. OTS employed the excess revenues to cover the OTR deficit during this transition period. Since 2013, OTR TSF rates have been increased to cover their full costs and PLT TSF rates have been decreased. In order to address the accumulated historic OTR deficit, a premium is added to the OTR costs and the collected revenue over and above OTR diversion costs and applied as a credit against PLT costs, effectively lowering the TSF rate.

2. Program Reserve Rebate: In operating the UTP, OTS has established a set of restricted reserves to mitigate risks of program disruptions and to support activities related to OTS’s diversion mandate. Following the Wind-Up direction provided by the Minister of the Environment & Climate Change to OTS, the organization has determined that the need for a portion of these restricted reserves will diminish as the UTP approaches the wind-up date of December 31st, 2018. OTS is therefore undertaking a process to draw down these reserves and apply the unrestricted funds to offset costs in tire classes identified as having contributed to the reserves. This process will have the effect of reducing the TSF rate for that tire class below the level that would be required simply based on the costs associated with diverting used tires from that class.

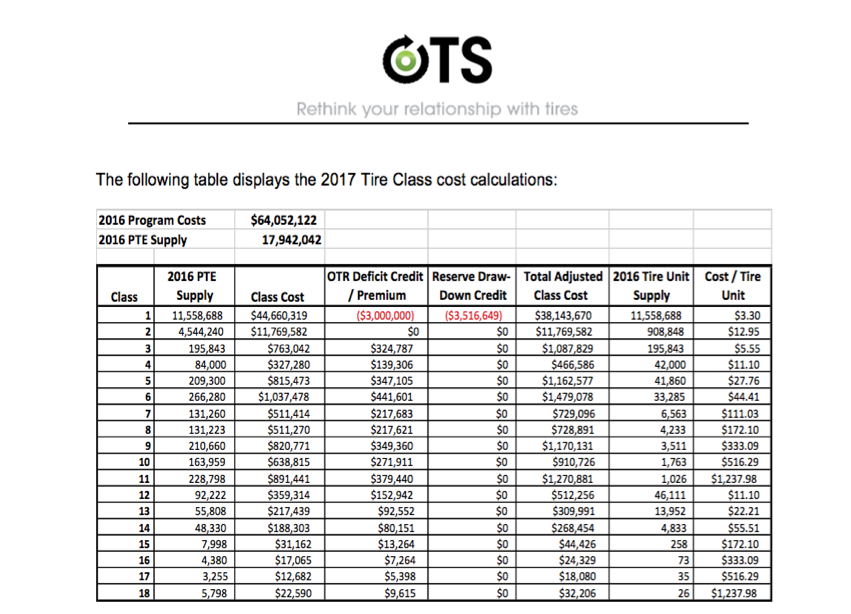

The following table, which can be viewed here, displays the 2017 Tire Class cost calculations.

Please do not hesitate to contact OTS with any questions regarding these revisions, either by e-mail at info@rethinktires.ca or by phone at 1-888-687-2202. We look forward to working with you to continue to deliver the Ontario Used Tires Program successfully.

Regards,

Andrew Horsman

Executive Director

{kind=link}